Data Action Layer October 28, 2021

Why KYC is Ripe for IDP

2020 marked another record-breaking year for doling out anti-money laundering (AML) fines, with more than $3.2 billion leveled worldwide against institutions that failed to meet compliance mandates, and 2021 is shaping up to be not that different. One of the common penalties was a result of inadequate compliance with know-your-customer (KYC) regulatory mandates.

Because of these steep fines, negative impact on reputation, and potential customer loss, many financial services firms turn to intelligent data processing (IDP) and workflow automation to help with their KYC efforts, with transformative results.

The changing face of KYC

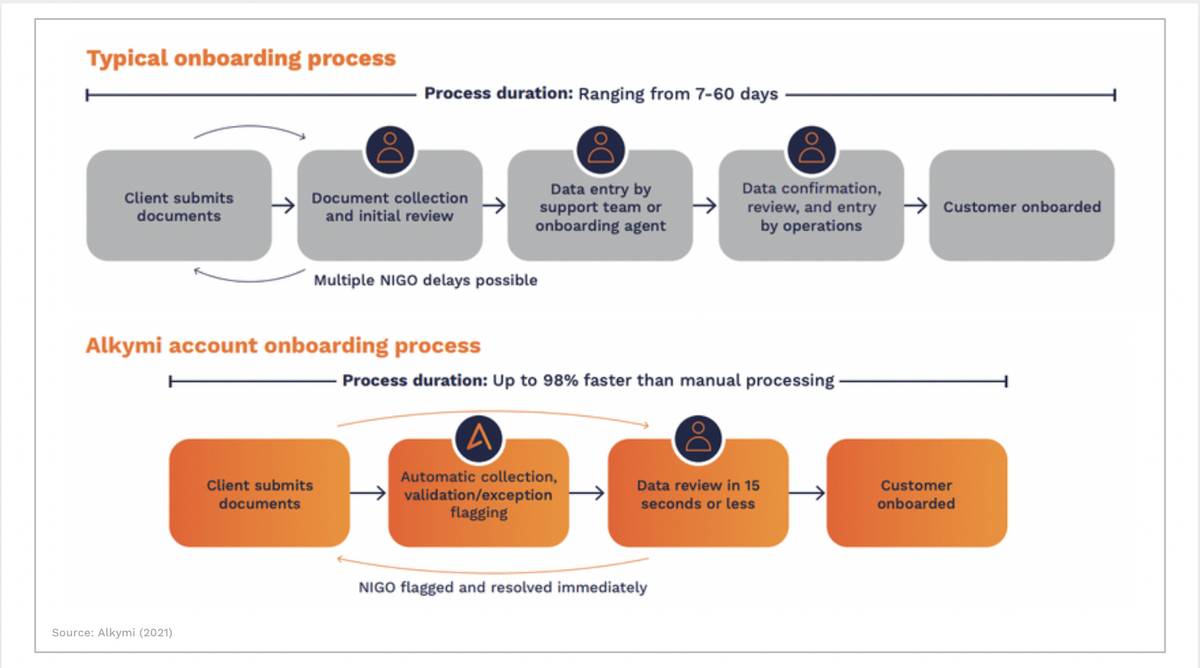

KYC is the aggregate of processes that financial institutions follow to establish a customer’s identity and ascertain that the source of the customer’s funds is legitimate. In addition to this upfront work, typically done during the client onboarding process, KYC also includes monitoring a customer’s ongoing activities to ensure no risks of illegal activity, specifically money laundering.

But as many financial institutions have found, at a high cost, that it can be almost impossible to comply with KYC without creating large, ever-growing operations teams. The challenge is three-fold:

First, the number of KYC regulations is growing—and existing ones are constantly changing. This means the type and amount of data that the institutions collect and analyze also expands exponentially. KYC, AML MiFID II, FTFCA, Dodd-Frank, EMIR, CRS…the list goes on and on. The rising cost of compliance and the vast amount of documentation required across the various mandates is staggering.

Second, the manual work required to extract the necessary details from this growing range of sources—some digital, some paper-based, some structured, some unstructured—is unsustainable without some form of automation. Until now, banks and other financial institutions resorted to hiring and training armies of people to perform the necessary due diligence work, which has significantly impacted their spending.

And third, the fact that the extracted data still has to be traceable to the source document makes it difficult to keep records up to date and easily auditable.

What does intelligent document processing have to do with KYC?

IDP can be used to extract relevant data from any kind of document—whether a structured database file or spreadsheet, or unstructured, like email or image. It uses artificial intelligence (AI) techniques such as computer vision (CV), natural language processing (NLP), and machine learning (ML) to determine which data to extract and what to do with it post-extraction. Market-leading IDP solutions will automatically do data validation, normalization, aggregation, and take actions, such as exporting the data into other systems.

Whereas many firms in the past depended on optical character recognition (OCR) technologies to digitize paper archives and other unstructured documents, they now are turning to IDP systems that seamlessly integrate into their own downstream systems for onboarding and due diligence.

How IDP relates to the three components of KYC

There are three related but separate components that make up KYC compliance. Here’s how IDP can help with each.

Customer identification program (CIP): The USA Patriot Act in 2001 was passed in response to the September 11 attacks as a way to protect U.S. financial systems, and it required all banks to create written CIPs that verified each customer's identity using credentials like name, date of birth, address, or social security number.

IDP helps with CIP by extracting all relevant data from documents of all types—birth certificates, social security cards, or driver’s licenses, and entering them into the KYC workflow.

Customer due diligence (CDD): CDD is the way that makes sure potential customers’ data is collected, that their identity is verified, and their risk profile completed. Customers are placed in one of two categories: simplified due diligence (SDD) and enhanced due diligence (EDD). SDD is used for accounts at low risk for money laundering. EDD is used for those at higher risk. When a customer is deemed to be higher risk, the financial institution needs to collect more information on them.

IDP helps with CDD in the same way as CIP by extracting all relevant data from documents of all types. IDP also can be used to digitize archives going back decades—something that financial institutions will eventually have to do—and cull out the meaningful data from that.

Continuous monitoring (or ongoing due diligence, ODD): Checking a customer once isn’t sufficient to satisfy KYC. Monitoring each customer’s activity is necessary to mitigate ongoing risks.

Again, IDP can pull data from all sorts of documents, including social media posts, emails, financial transactions, even handwritten notes, to ensure that customers stay within parameters over the long term.

Critical IDP features for successful KYC

- Flexible: Precisely because regulatory mandates are constantly evolving, the IDP solution you choose must make it possible to easily update business rules, form fields, and document requirements in response.

- Auditable: When choosing an IDP solution to extract data from documents—including both digital and paper ones—and then automatically feed it into the onboarding process, for example, you need to make sure you have a clear trail to the sources. That way, you’ll always know where the data originated and can verify it during audits.

- Easy to use: Because of the fast-moving and rapidly changing nature of KYC regulations and processes, you don’t want to create bottlenecks waiting for the IT department to reconfigure or adjust your IDP solution. It should be easy enough to learn and use so that your business users can make all the necessary changes themselves.

Making an impact

By deploying a leading IDP solution—capable of working with both structured and unstructured data and providing a clear, auditable trail back to the source material—banks and financial institutions are making strides towards creating a well-run KYC program. And with benefits like lowered fraud rates, better customer data, improved customer onboarding experiences, and greater transparency, it’s no wonder that the BSFI sector is turning to IDP to move the needle for their business.

Ready to boost your profitability? Get a demo with our experts today to see how Alkymi can transform your KYC process.

More from the blog

Alkymi at the SimCorp Global Summit 2025

by Maria OrlovaHighlights from Alkymi at the SimCorp Global Summit 2025

Alkymi Wins A-Team Innovation Award 2025

by Harald ColletAlkymi wins Most Innovative Unstructured Data Management Project at the A-Team Innovation Awards 2025

Human-in-the-Loop: The Essential Partnership Powering Successful AI

by Keerti HariharanDiscover why AI still needs human insight. Explore how Human-in-the-Loop (HITL) ensures accuracy, trust, and success in real-world AI workflows.